[ad_1]

Following a comparatively quiet week when it comes to financial information and occasions, the highlight now turns to 3 main central banks: the Federal Reserve, the European Central Financial institution, and the Financial institution of Japan. With traders anticipating just one extra hike by the Fed, the main target can be on whether or not officers will sign the tip of this mountaineering cycle, whereas with a number of ECB members pushing again on a September hike, will probably be fascinating to see whether or not Lagarde has additionally modified her stance. As for the BoJ, Governor Ueda’s newest remarks added to the chance of no motion.Will the Fed sign the tip of this tightening campaign?

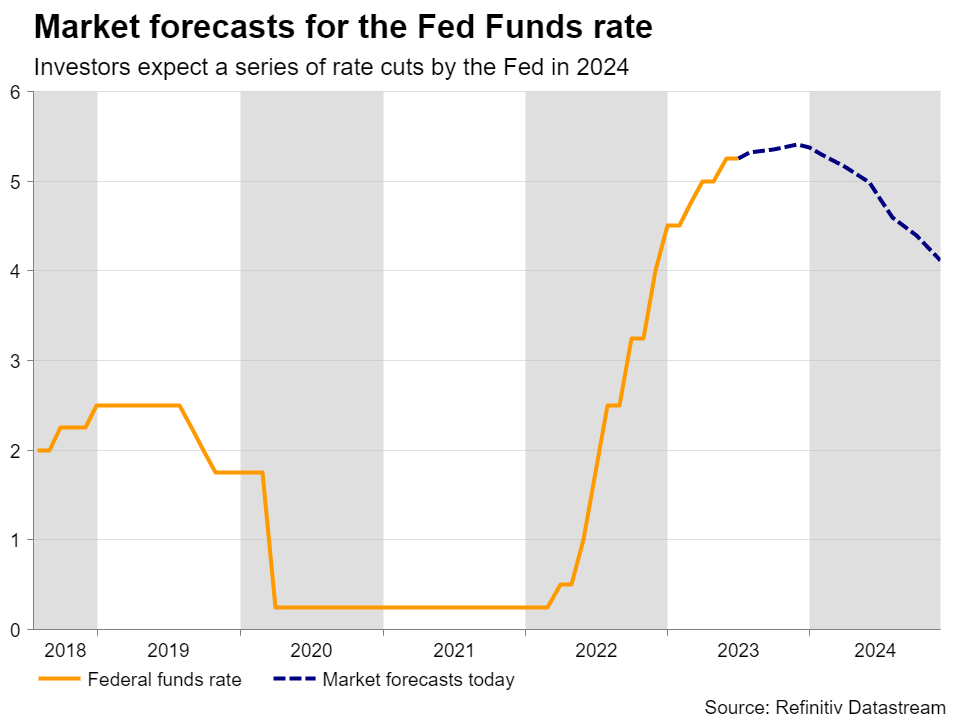

Following the greenback’s tumble final week because of the larger-than-expected slowdown in shopper and producer costs, market contributors have change into extra satisfied that the Fed will ship just one extra hike earlier than it ends this tightening campaign, whereas they elevated their Fed lower bets for subsequent yr.

The final time they met, Fed officers hit the pause button, however the determination had a hawkish taste, with the ‘dot plot’ pointing to 2 extra fee will increase and Fed Chair Powell pushing again on fee lower expectations by saying that any reductions are “a few years out.” Though traders weren’t satisfied again then and neither when Powell testified earlier than Congress, they started lifting their implied path after the Fed chief appeared at a panel dialogue organized by the ECB in a hawkish go well with.

However that was solely till final week’s inflation information. Due to this fact, Wednesday’s FOMC determination might appeal to particular consideration as traders can be desirous to get a clearer image concerning the Fed’s future plan of action. Given {that a} 25bps hike is sort of priced in, ought to it materialize, the highlight is prone to flip to the accompanying assertion for hints as as to whether this was the final hike or whether or not charges may go larger.

With core inflation greater than double the Fed’s 2% goal, Powell and co are unlikely to sign that this tightening campaign has ended. They might reiterate the view that the struggle in opposition to inflation will not be over, whereas on the press convention, Powell may as soon as once more push in opposition to fee lower expectations.

Nevertheless, it stays to be seen whether or not one other spherical of hawkish rhetoric can be sufficient to persuade market contributors sufficient to reduce their fee lower bets, as a few of them could also be holding the view that prior hikes may nonetheless work in bringing inflation additional down within the coming months.

They might get an thought of the place inflation could also be headed from the costs subindices of the preliminary PMIs for July, due out on Monday, whereas Friday’s core PCE index may additionally have an effect on their view after the gathering.

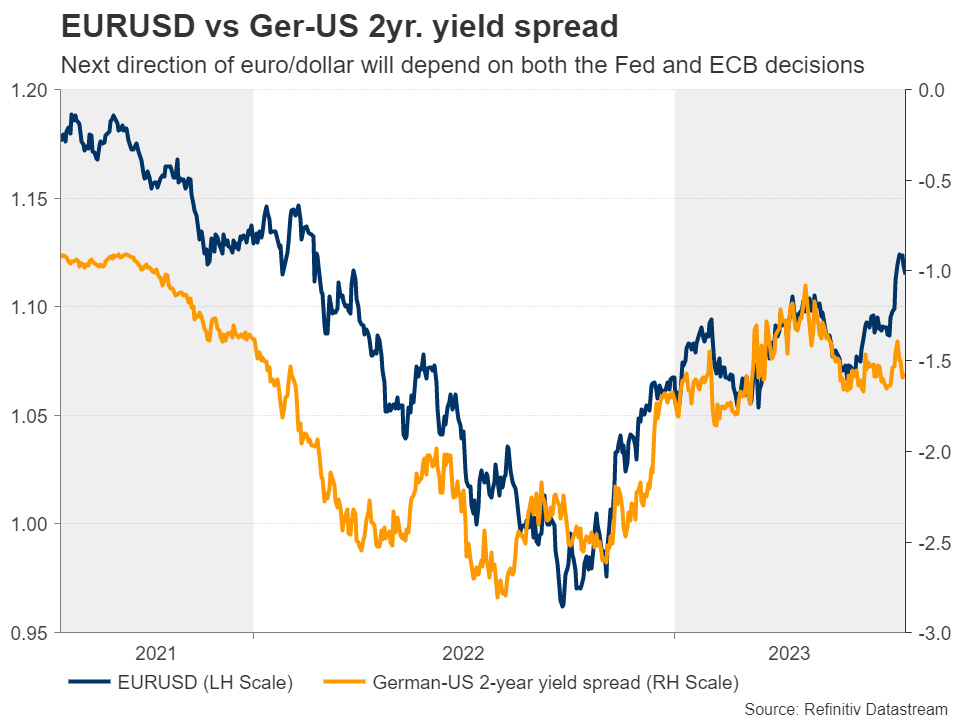

ECB to hike, focus to activate Lagarde’s remarksUp till this week, the ECB was seen as way more hawkish than the Fed, anticipated to ship two extra quarter-point hikes this yr and no cuts in any respect thereafter. That stated, with a number of ECB policymakers arguing {that a} September hike will not be a accomplished deal, that image has modified. Sure, there are nonetheless almost two quarter-point hikes priced in, however merchants now imagine that rates of interest within the Euro space will finish subsequent yr 25 foundation factors under present ranges. In different phrases, conditional upon two hikes being delivered this yr, the market expects three fee cuts in 2024.

That pricing could also be affected by the preliminary PMIs due out on Monday, and though a July hike appears a accomplished deal, indicators that the Eurozone is dropping extra financial steam may immediate hypothesis of a softer language within the assertion accompanying the choice. The massive query although could also be whether or not ECB President Christine Lagarde has additionally softened her stance or whether or not she is going to seem in her hawkish go well with once more, dismissing the Eurozone’s financial slowdown and prioritizing getting inflation in verify.

If Lagarde sticks to her weapons the euro is prone to achieve and maybe prolong these beneficial properties on Friday if preliminary CPI information means that inflation in Germany is stickier than beforehand thought.

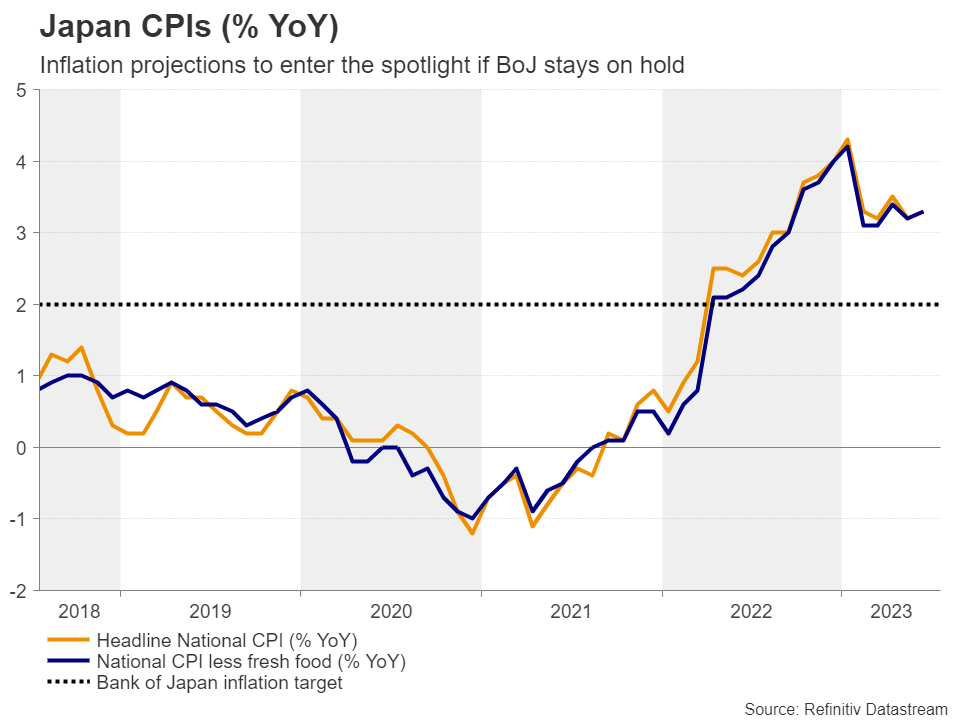

BoJ seen on maintain as Ueda pushes again on shift expectationsOn Friday, the central financial institution torch can be handed to the BoJ. After testing the psychological, intervention-debated, 145.00 stage, greenback/yen got here underneath robust promoting curiosity, hitting a backside at round 137.25, earlier than rebounding once more. The slide was not solely the results of a weaker greenback but in addition a stronger yen as market contributors might have began elevating bets that the BoJ may tweak its coverage at this gathering.

Nevertheless, earlier this week, Governor Ueda reiterated his remarks that there’s nonetheless far to realize the two% inflation goal sustainably and stably, signaling dedication to take care of ultra-loose coverage for now. Merchants have began scaling again their bets of an imminent coverage shift, permitting greenback/yen to rebound. That stated, even when the Financial institution doesn’t act at this gathering, market contributors could also be within the new inflation projections as they could attempt to estimate the size of the space Ueda is referring to.

If these projections are revised notably larger, the yen might achieve, even when there isn’t a coverage shift now, as they’ll begin speculating for a normalization step maybe on the subsequent gathering. The other could also be true if Ueda and his colleagues place extra emphasis on sustaining present coverage on account of inflation being primarily pushed by costly imports somewhat than home demand.

Australia CPIs, UK PMIs, and tech earningsElsewhere, Australia’s CPI information for Q2 are popping out on Wednesday. Simply this Thursday, the employment information for June got here in higher than anticipated, growing the chance for an additional hike on the RBA’s August assembly. At the moment, traders are evenly break up on whether or not the Financial institution ought to hike or not, and the CPIs have the potential to tip the dimensions.

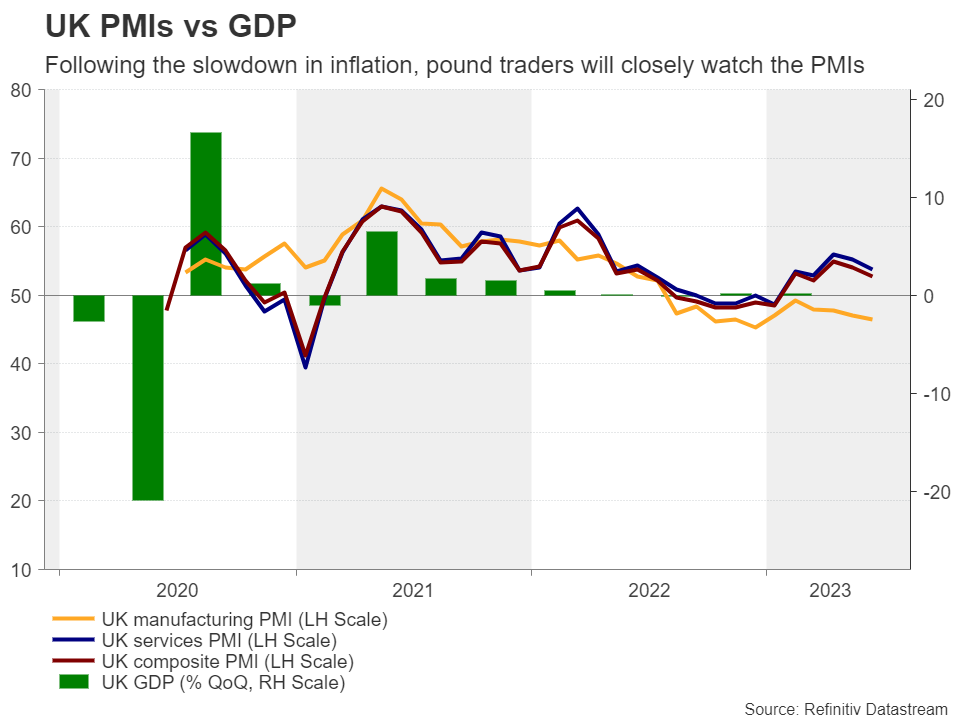

For the pound, the week begins and ends on Monday with the preliminary PMIs for July. The British foreign money suffered this week on the again of a larger-than-expected cooling in UK inflation for July, prompting market contributors to ditch bets of one other double hike in August and take off the desk a few of the foundation factors value of hikes they had been anticipating thereafter. So, ought to the surveys reveal that costs charged throughout July rose at a slower tempo than in June, the pound may endure extra as merchants reexamine the ultra-hawkish BoE narrative.

Lastly, on the earnings entrance, we get the outcomes from tech giants Alphabet (NASDAQ:), Microsoft (NASDAQ:), Meta and Amazon (NASDAQ:).

[ad_2]

Source link