[ad_1]

J. Michael Jones/iStock Editorial through Getty Photographs

Firstly of 2020, I revealed “United Leases: A Pure-Play Worth Alternative Forward Of The Building Growth,” detailing my constructive long-term view on United Leases (NYSE:URI). Since then, the inventory has risen by ~187% due to an enormous earnings improve and valuation. As anticipated, the corporate benefited from a considerable improve in business and residential development spending. At the moment, the corporate performs very effectively and instructions a a lot larger valuation as buyers are not discounting threat on the inventory. US development spending stays excessive, encouraging the agency’s development. Nevertheless, shifting financial winds doubtlessly threaten the corporate.

URI is probably going reaching its cyclical peak as developments counsel an impending sharp and extended slowdown in US development exercise. From a valuation standpoint, it seems that many buyers are forgetting the cyclical actuality of the corporate. In different phrases, URI is not buying and selling at an affordable valuation given its inevitable cyclical publicity. As development spending ranges roll over, United Rental’s earnings could fall shortly. Additional, the development tools scarcity, which has dramatically benefited URI, seems more likely to gradual quickly as manufacturing ranges from many development tools manufacturing corporations rise dramatically from slowing demand.

That mentioned, the corporate has a robust steadiness sheet with ample liquidity, permitting it to beat headwinds higher than earlier than. United Leases stays highly regarded amongst many buyers and deserves detailed evaluation given its robust efficiency. Moreover, URI is in a essential technical place because the inventory returns to its all-time-high value within the $450 vary it reached final February. For my part, that technical “double high” place, mixed with the corporate’s fundamentals, factors to impending detrimental value motion. Nevertheless, some elements impacting the agency might trigger it to rise to a brand new excessive.

Building Tailwinds Develop into Headwinds

United Leases is extremely uncovered to financial circumstances. For one, development exercise adjustments dramatically with macroeconomic occasions with important dependence on rate of interest ranges. Moreover, a decline in development exercise has an uneven detrimental affect on United Leases as a result of rental demand is partially pushed by extra development exercise. In different phrases, URI’s merchandise are in larger demand when development exercise rises sufficient that contractors want further tools. Thus it doesn’t essentially take a big decline in development exercise to have a big detrimental affect on URI’s gross sales.

In February 2020, after I was very bullish on the corporate, rates of interest had been meager, inflicting development exercise to rise shortly. Certainly, the extra appreciable decline in rates of interest in 2020 as a consequence of Federal Reserve stimulus efforts was sufficiently giant to trigger development spending to rise throughout in any other case poor financial circumstances. At the moment, rates of interest are the very best in a long time, inflicting a pointy (and rising) decline in business property values and transaction volumes. Building prices are considerably elevated immediately as a consequence of inflation, significantly in development labor, so builders can’t afford a 30-40% decline in business property values.

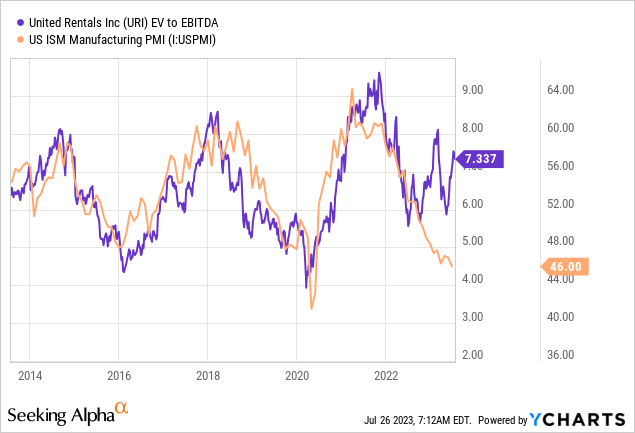

Buyers shouldn’t be caught off guard by the robust efficiency of United Leases this 12 months. Considerably, the corporate’s efficiency lags behind development spending. Building spending lags behind adjustments in property values, and adjustments within the property market lag behind fluctuations in monetary markets. Thus, there’s a super lag between adjustments in monetary situations and United Leases’ earnings; nevertheless, the connection is traditionally very strong. Probably the most fascinating patterns exhibiting that is the correlation between URI’s “EV/EBITDA” ratio and the US manufacturing PMI:

The US Manufacturing PMI is a sturdy future indicator of adjustments in manufacturing enterprise exercise. Key measures embrace adjustments so as volumes, inventories, employment, and so on. Ranges beneath 50 counsel a detrimental development in these figures for a lot of manufacturing corporations. Traditionally, the PMI is a strong main indicator of actual GDP development. The robust relationship between the PMI and URI’s valuation shouldn’t be coincidental. When the PMI is powerful, URI will probably see its earnings rise quicker, inflicting its valuation to extend (providing a premium for future earnings). When the PMI is low, URI is more likely to see a decline in earnings, so its valuation contracts to low cost an impending drop in gross sales. At the moment, we’re seeing an abnormality as URI’s “EV/EBITDA” stays elevated, however the PMI is signaling a big impending decline in its gross sales – signaling an overvaluation for URI.

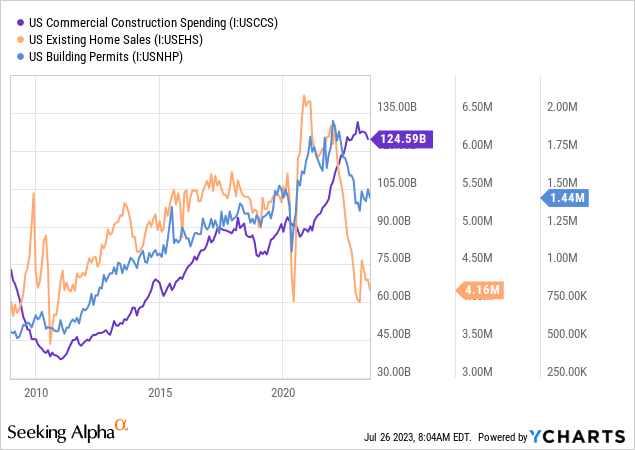

In fact, the development business has been one of many strongest within the manufacturing sector since 2020. Accordingly, buyers in URI might even see its robust momentum as an indication that its earnings is unlikely to face cyclical pressures. For my part, that momentum can create an extended “lag” between the broader financial cycle and development exercise, but it surely won’t negate it. Current dwelling gross sales are falling towards 2008 recession lows immediately. Constructing permits and business development spending are additionally beginning to decline, however they continue to be elevated in comparison with dwelling gross sales. See beneath:

Business property gross sales are additionally extraordinarily low immediately as a consequence of tighter lending and occupancy declines. Thus, there’s a strong detrimental development in gross sales exercise for residential and business area builders, even when builders haven’t completely accepted that actuality. Builders proceed to construct at important charges, probably as a result of they deliberate tasks when rates of interest had been a lot decrease and the potential earnings a lot larger. Nevertheless, I consider they run an elevated threat of constructing at super losses, significantly on extra important properties in city areas. Accordingly, United Leases ought to nonetheless see near-peak gross sales over the approaching quarter or two. Nonetheless, I anticipate that determine to say no dramatically in 2024 as builders cut back exercise in response to property costs and gross sales quantity declines.

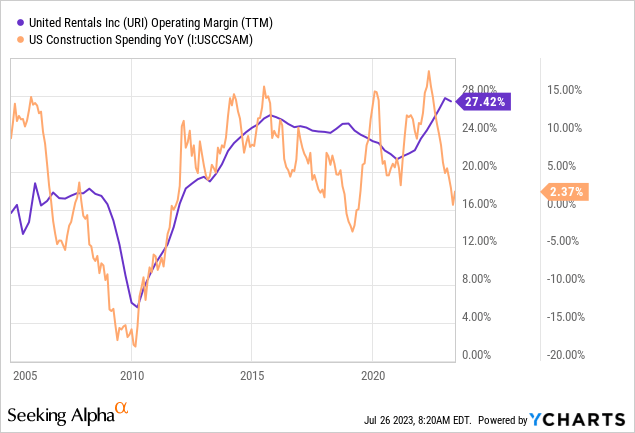

United Leases has additionally benefited from a scarcity of development tools. In 2020-2022, demand for development equipment rose dramatically as builders ramped up exercise. Nevertheless, the compelled manufacturing halt from lockdown measures wreaked havoc on the equipment provide chain. As demand for development tools rose whereas provide declined, United Leases has seen a pointy improve in its revenue margins because it expenses larger costs. As you possibly can see beneath, there’s a normal relationship between URI’s working margin and the expansion of development spending:

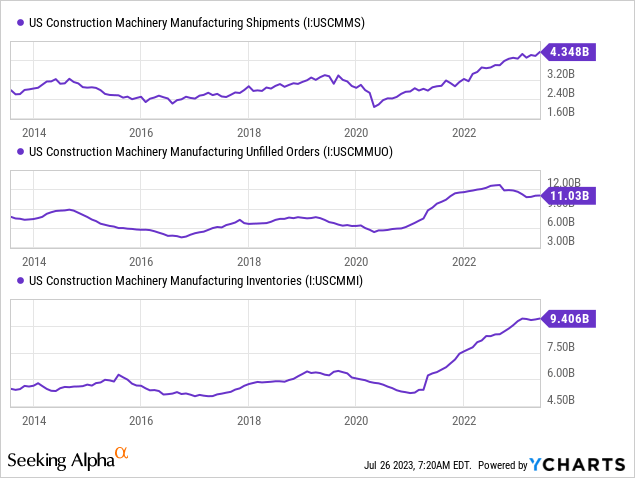

When development spending rises shortly, it’s likelier that equipment falls into quick provide, permitting URI to spice up its costs. Conversely, declines in development spending pressure URI to cut back its costs and hamper its margin or threat incomes nothing on its belongings. Building spending has slowed over the previous 12 months, however I firmly consider it’ll see a extra appreciable decline, as evidenced by the sharp fall in property market gross sales. Additional, the provision of development equipment is rising in a short time, as seen in manufacturing shipments, unfulfilled orders, and inventories:

These knowledge are extremely related for firms like Caterpillar (CAT) and others that produce development tools. Because the scarcity grew, these firms had shallow stock ranges from 2020-2021. Nevertheless, their inventories have doubled since then and are over 50% above their regular maximal ranges immediately, indicating a possible glut ought to orders decline. Cargo ranges stay very excessive, indicating that demand is strong, implying elevated competitors for United Leases. Lastly, unfulfilled orders are beginning to wane, that means manufacturing ranges are rising quicker than demand.

Total, I consider it’s clear that United Leases is headed into a pointy cyclical slowdown. Its state of affairs immediately is sort of the alternative of its place after I grew to become bullish over three years in the past. Rates of interest (the first demand leaver) are a lot larger, inflicting immense strains within the property market, significantly for extra important buildings. Building exercise indicators are excessive, however they’re beginning to gradual and may fall quicker in response to property value and gross sales fluctuations. Additional, the provision of development tools is rising very quick as factories lastly increase output to satisfy demand; nevertheless, they seem more likely to create a glut out there as manufacturing of development tools is now rising quicker than demand, resulting in a listing buildup. By 2024, I consider these elements will inevitably result in a pointy decline in United Leases’ gross sales and working margins.

What’s URI Value At the moment?

To me, it’s clear that URI is headed for a cyclical slowdown. With that in thoughts, the subsequent key questions are how appreciable that deceleration shall be, how lengthy it’ll final, and whether or not or not long-term demand will assist restoration. These key elements are troublesome to find out immediately as we’re solely on the preliminary stage of a slowdown. That mentioned, business property valuations are anticipated to say no at a document tempo, in the end stemming from document will increase in rates of interest final 12 months. Additional, robust normal GDP indicators such because the PMI and the yield curve (which often inverts ~18 months earlier than a recession) are on the lowest ranges since 2008, with the yield curve being essentially the most inverted because the Nineteen Eighties.

Whereas not excellent, these knowledge point out a steep recession that will final for a while. Certainly, the US financial system faces important boundaries it’s lastly being compelled to beat. These embrace continual unsustainable debt ranges in each private and non-private debt markets, which is now a bigger difficulty as rates of interest usually are not near-zero. Years of decline within the complete US manufacturing base created immense inflationary dependence on imports, primarily as a result of important deterioration in manufacturing facility labor productiveness since ~2010.

The checklist goes on and factors to the truth that the US, and certain a lot of the Western world, requires an financial pressure to enhance effectivity and cut back the numerous monetary and financial excesses created over the previous a long time. Whereas measures like QE, fiscal deficits, and others have managed to delay fixing these points since ~2008, I consider that it can’t be delayed way more as a consequence of dangers related to the US greenback and commerce imbalance.

These elements usually are not straight related to development, however they’re appropriate for long-term GDP development, which is the first driver of development exercise. Based mostly on this, I’m biased towards the view that United Leases is dealing with a comparatively sharp and extended slowdown because the US slows development exercise in response to quite a few different points.

The US will probably must develop development in the long term as a consequence of dilapidated infrastructure and aged properties and buildings. There’s undoubtedly a necessity for better development within the US, however the US financial system doesn’t have the essentially giant manufacturing base to assist it, with most development uncooked supplies (and, to a big extent, labor) coming from overseas nations. So long as that difficulty stays an element, I don’t consider the US financial system can assist the development exercise its infrastructure and buildings require. In the long term, URI could profit from a development growth, however that won’t happen till the 2030s as it’ll take time (and certain in depth bipartisan authorities assist) for that to occur, and up to date efforts are probably not near carrying out that.

Traditionally, URI’s gross sales decline by round 20-35% throughout recessions whereas its working margins contract by ~10%. Assuming it faces a slowdown much like 2008, however not as giant, I anticipate its gross sales to fall to ~$9.3B annualized or 25% decrease. Additional, its working earnings may decline to round $1.4B as its working margins slide to ~15%, a conservative estimate as they fell all the best way to ~6-7% in 2010. The corporate has round $500M in curiosity prices as a consequence of its capital depth. Its curiosity prices could rise because it’s increasing its capital base and rates of interest rise, however I cannot assume that given it has not elevated materially since 2022. Accordingly, I anticipate URI’s pre-tax earnings to fall to an estimated $890M and its internet earnings to ~$667M (25% tax price), translating to a ~$9.8 EPS.

That determine is my estimate for absolutely the trough for URI’s earnings in a recession. After a slowdown, I anticipate earnings to rise slowly to regular ranges however they might not return to present ranges for a very long time as a consequence of macroeconomic circumstances. As such, I consider a 20X “P/E” on that “trough” EPS is cheap, equating to a value goal of ~$196, beneath half of URI’s present worth. That mentioned, the corporate was buying and selling nearer to $150 for all the decade earlier than 2020, and its standing has not basically modified since, so I don’t consider my very bearish outlook is unreasonable.

Lastly, URI could also be a brief alternative as a result of extent of its overvaluation and its “double high” technical positioning. Even when my basic view is simply too bearish, it appears arduous to justify the corporate’s worth in gentle of shifting financial developments. Since URI has carried out so effectively, it has low quick curiosity, no materials borrowing prices, and comparatively low implied volatility for these trying to cut back threat with put choices. The chief threat with betting towards URI is that it breaks its all-time excessive right into a speculative rally, which is feasible, however to me unlikely. That threat may be managed with a cease lack of round $470-$500. Admittedly, as a result of “lag issue” from the property market to development exercise, URI’s EPS could take longer than anticipated to say no; nevertheless, I might be stunned if that doesn’t happen by mid-2024. Total, I consider the timing for short-selling URI is good (as seen within the irrational exuberance round URI). Nonetheless, there are inevitable dangers with getting into such speculative trades whereas they’re in an early stage.

[ad_2]

Source link

{kind=link}