[ad_1]

Markets have been taunted by shifting Fed expectations over the previous week and there’s prone to be extra anguish for buyers within the subsequent few days as essential payrolls and inflation numbers are developing. The August jobs report and PCE inflation readings can be intently watched amid indicators the US financial system is beginning to lose steam quick. The Eurozone financial system goes via a fair rougher patch, placing the highlight on flash CPI figures. China has been one other supply of concern and its PMI prints for August can be necessary too. NFP report and PCE inflation to lift the stakes

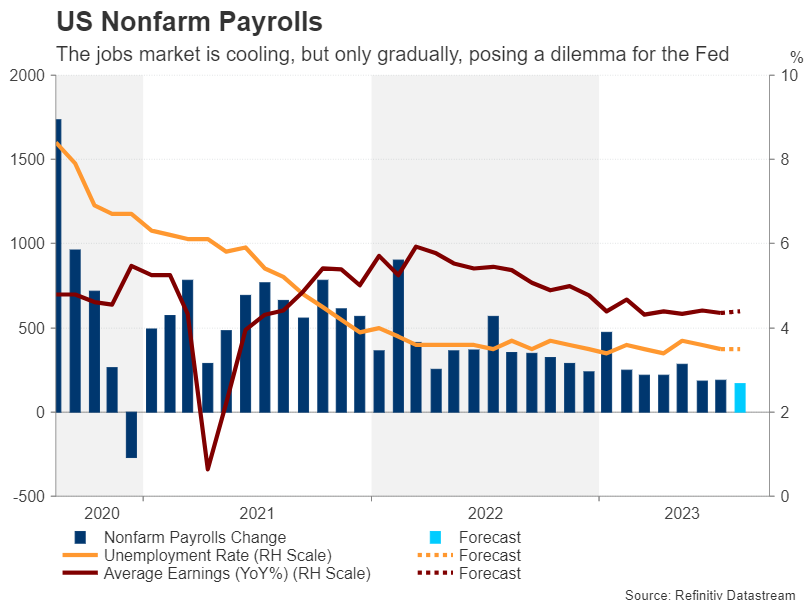

It is payrolls week in the USA and the August numbers can be eagerly awaited on Friday as, aside from some indicators already that jobs development is slowing, the newest S&P International PMI survey raised a couple of alarm bells about hiring situations. Nonfarm payrolls are projected to have elevated by 170k in August, moderating from the 187k jobs added in July.

The unemployment charge is predicted to carry regular at 3.5%, whereas common hourly earnings development can also be forecast to stay unchanged at 4.4% y/y in August.

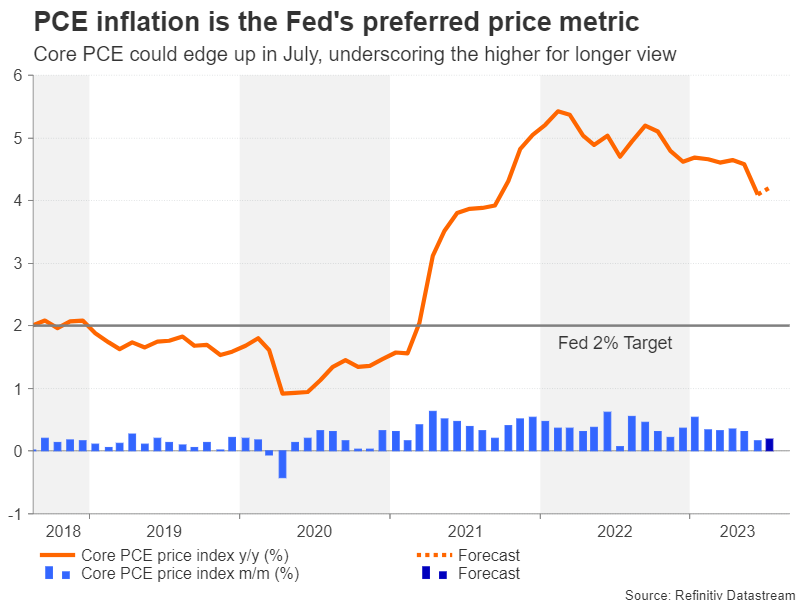

Additionally attracting quite a lot of consideration is Thursday’s private earnings and outlays report, which comprises the all-important core PCE value index. With each private earnings and private consumption holding up surprisingly effectively in opposition to the backdrop of rising borrowing prices, one other strong studying for August would ease worries a couple of slowing financial system. What has been extra of concern, nonetheless, is the stickiness of the Fed’s favorite inflation gauge.

Though core PCE did lastly take a dive in July to fall to 4.1% y/y, that’s nonetheless double the Fed’s goal of two%. Moreover, core PCE might edge as much as 4.2% in July, so these buyers hoping for additional declines on this specific metric are prone to be dissatisfied.

But, with the financial dangers tilted considerably extra in the direction of a recession than a delicate touchdown after the PMI releases, if the above indicators are broadly higher than anticipated, it’s unlikely that charge hike odds would rise very considerably. Then again, an general delicate and even poor set of information may lead buyers to additional up their charge minimize bets for subsequent yr, punishing the US greenback however most likely boosting Wall Road.

Wrapping up the US agenda on Friday would be the ISM manufacturing PMI, which can get to have the ultimate say on how markets shut for the week. It’s anticipated to come back in at 46.6 for August, a really modest enchancment over the prior month.

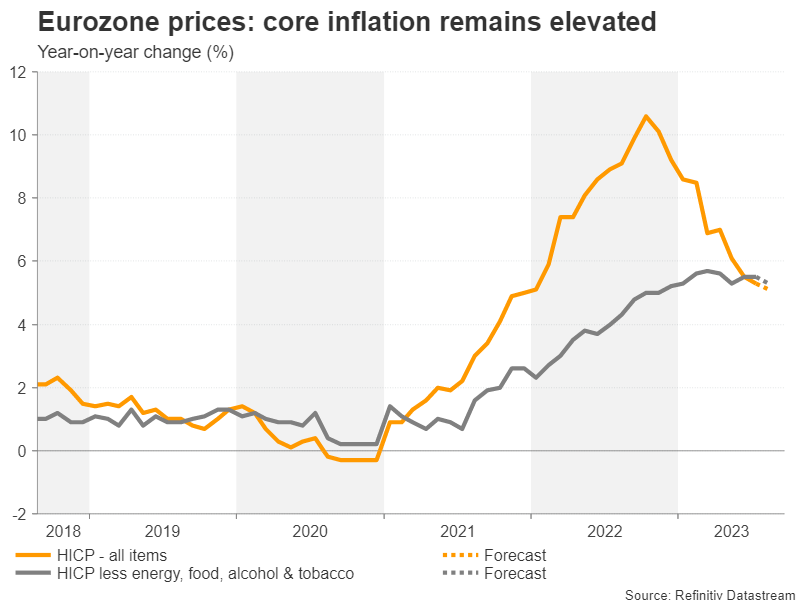

Will Eurozone inflation hold falling?Throughout the pond, recession fears are heightened much more so, as there seems to be no reduction for European companies recently. Manufacturing exercise did enhance barely in August, however companies output slumped deeper into contraction territory. With rates of interest at a document excessive for the reason that euro’s inception, power costs rising once more and demand weakening in key export markets such because the US and China, one of many few issues Europeans can rejoice about is that inflation is on the way in which down.

The flash estimates for August are due on Thursday and may present additional declines. The headline charge of CPI is predicted to dip from 5.3% to five.1% y/y, whereas core CPI that strips out meals, power, alcohol and tobacco costs is forecast to ease from 5.5% to five.3% y/y.

The European Central Financial institution has repeatedly confused that getting core CPI right down to 2% is its important precedence and can possible relay that message within the minutes of the July assembly that can be revealed on Thursday. Nevertheless, a much less hawkish-than-anticipated tone is feasible because the current deceleration in development is elevating doubts in regards to the want for additional charge will increase.

The euro might halt its slide and agency considerably ought to charge hike bets for September, which in the meanwhile is a coin toss, be ratcheted up from any upside surprises. However even then, the positive factors can be restricted as the chance of a extra extreme downturn would additionally rise.

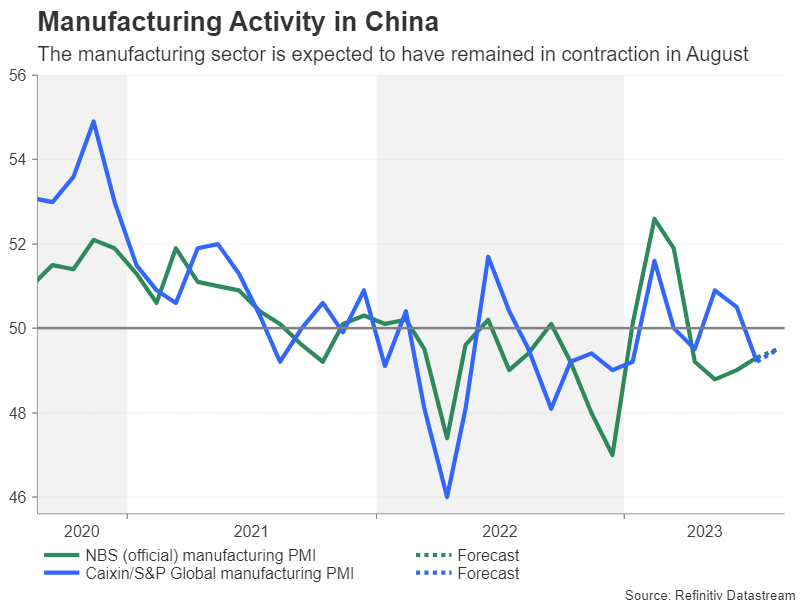

Battered eyes Chinese language PMIs and native CPIsAmid frustration about China’s drip-feed stimulus, bulletins on new help measures have change into virtually a every day prevalence. But, for the markets, a one-off bazooka is seen as having an even bigger impression. Within the absence of 1, all buyers can do is to search for indicators that the incremental coverage tweaks are beginning to generate some momentum within the financial system.

There might be some clues of this on Thursday when China experiences its manufacturing and non-manufacturing PMIs for August. The Caixin manufacturing PMI will observe on Friday.

The Australian greenback, which is seen as a liquid proxy for China-related dangers, has taken fairly a beating recently following a collection of downbeat Chinese language knowledge. China’s slowdown is already being felt throughout the Australian financial system as pointed by the current dismal PMIs.

Subsequent week, the main target can be on home barometers, comprising July retail gross sales (Monday), month-to-month CPI prints (Wednesday) and Q2 capital expenditure (Thursday).

In current conferences, the Reserve Financial institution of Australia had change into extra involved about development than inflation. If the annual CPI charge maintains a downward course in July, the RBA would have little incentive to hike charges once more, and until there’s a turnaround in threat sentiment, the aussie appears poised to stay below stress.

[ad_2]

Source link