[ad_1]

hapabapa/iStock Editorial by way of Getty Pictures

Firm Overview

Costco operates company-owned warehouses and e-commerce web sites based mostly on the idea of providing its members low costs on a restricted number of nationwide manufacturers and personal label merchandise in all kinds of classes, which generates excessive gross sales volumes and speedy inventory turnover. At present, Costco has over 838 warehouses.

We are going to analyze Costco’s enterprise mannequin and valuation to grasp why it’s at present a maintain.

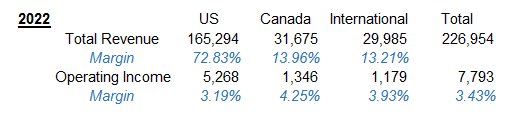

Costco’s income and working earnings margins (Authored utilizing firm monetary knowledge)

America is by far the most important area for Costco, accounting for 73% of whole income and three.19% of whole working earnings. Canada is the second-largest area, producing 14% of whole income and 4.25% of working earnings. The worldwide area is the smallest, with a 13% share of whole gross sales and three.93% of working earnings. Which means that the US is the most important area for Costco, however Canada is probably the most worthwhile area.

Rivals & Multiples

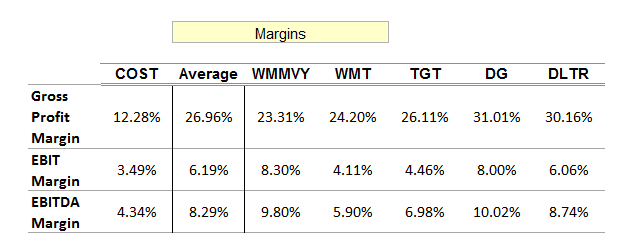

Business Margins (Created by the writer utilizing knowledge from Looking for Alpha)

Costco’s business is extremely aggressive, with components reminiscent of value, merchandise high quality and choice, location, comfort, distribution technique, and customer support all taking part in a task.

As we will see above, Costco operates with considerably decrease margins than most different retailers. It’s because Costco’s technique is to offer its members with a variety of high-quality merchandise at costs which can be constantly decrease than elsewhere. Costco carries lower than 4,000 lively stock-keeping items (SKUs) per warehouse in its core warehouse enterprise, considerably lower than different broadline retailers. Costco additionally typically sells stock earlier than it’s required to pay for it, even whereas benefiting from early cost reductions.

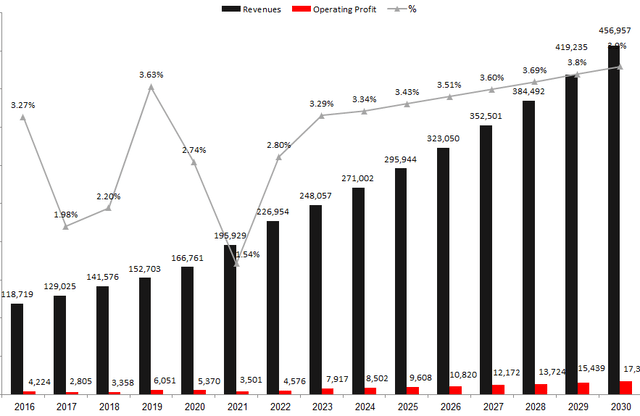

Costco Estimates Working Revenue Margin (Authored utilizing Costco monetary knowledge and the writer’s projections)

As may be seen within the graph, Costco’s working revenue margin lately has not been notably resilient, as a result of important affect of COVID-19. Nonetheless, I consider that Costco’s working revenue margin will present resilience and a few progress within the coming years, pushed by its enlargement in e-commerce.

Costco Membership

Costco gives two kinds of membership: Gold Star and Enterprise. Gold Star memberships can be found to people, whereas Enterprise memberships are restricted to companies. Costco’s annual payment for these memberships is $60 in the US. In the US, members may also improve to an Government membership for an extra annual payment of $60. Government members earn a 2% reward on certified purchases (as much as $1,000 per yr), which may be redeemed at Costco warehouses. In 2022, Government members totaled 29.1 million and represented 57% of paid members in the US and Canada and 22% of paid members in Costco’s worldwide operations. Government members accounted for about 71% of Costco’s worldwide internet gross sales in 2022.

Costco has a transparent technique: it makes most of its cash from membership charges, not from promoting items. Costco’s revenue margins on the merchandise it sells are extraordinarily skinny, a lot thinner than these of conventional grocery shops. As a substitute, Costco depends on membership charges to generate earnings.

You recognize, most of their internet earnings comes from memberships payment income so final yr, 92% of their whole internet earnings got here within the type of memberships payment income.

– Garrett Nelson, Senior Fairness Analysis Analyst, CFRA Analysis –

Costco is extraordinarily targeted on maintaining its members pleased. The corporate has been refusing to boost costs on items to enhance margins on gross sales, simply to maintain its prospects coming within the door.

One of the simplest ways to see the success of Costco’s membership program is to have a look at its member renewal charge, which was 93% within the U.S. and Canada and 90% worldwide on the finish of 2022.

Costco Memberships (Costco’s monetary report)

The energy of Costco’s membership mannequin is clear in its year-over-year progress. I consider that this progress is a testomony to the satisfaction of Costco’s prospects, and I anticipate it to proceed within the coming years.

Valuation

I’ve two valuation fashions for Costco: one based mostly on seasonality and one based mostly on the expansion charge of places over the previous six years. Let’s begin with the primary mannequin.

The seasonal valuation mannequin for Costco accounts for the truth that the corporate’s gross sales range all year long, with increased gross sales within the fourth quarter (which incorporates the vacation season) and decrease gross sales within the first quarter. The mannequin makes use of historic gross sales knowledge to estimate these seasonal patterns, after which calculates the corporate’s valuation based mostly on these patterns.

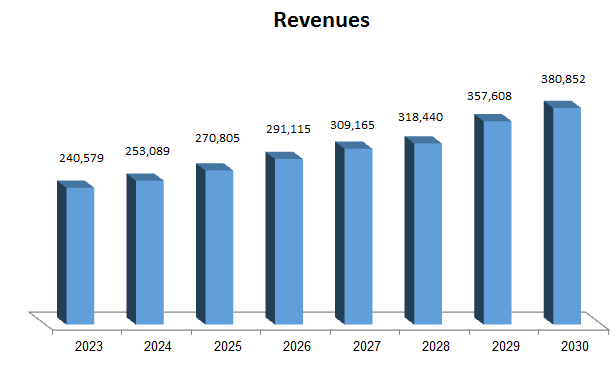

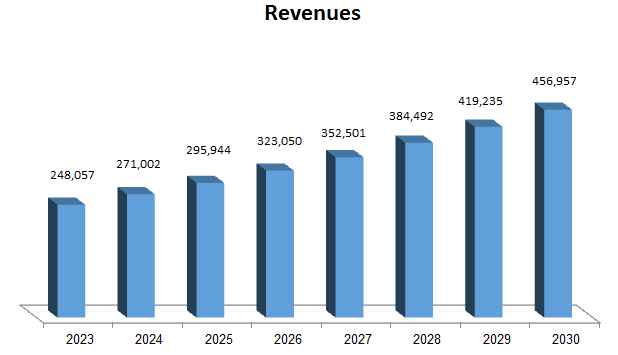

Price’s Estimates Income (Authored utilizing Costco monetary knowledge and the writer’s projections)

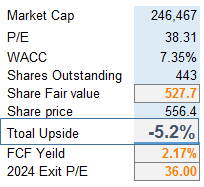

I used a reduced money circulate (DCF) methodology to evaluate COST’s truthful worth. I assumed that the corporate’s income would develop at a compound annual progress charge (CAGR) of 6.8% between 2023 and 2030, based mostly on the robust enlargement of warehouses and progress within the memberships, which is within the line decrease than the consensus. That is decrease than the corporate’s historic progress charge (OTC:CAGR)) of 11.4% between 2016 and 2022, however nonetheless very spectacular.

The valuation displays a 2024 P/E of 36x, based mostly on my EPS projection for 2024. That is according to the consensus.

Creator’s assumption (Created and calculated by the writer)

Primarily based on this mannequin, I estimate the corporate’s truthful worth to be $527.7 per share.

The Second mannequin

Warehouses enlargement (Authored utilizing Costco monetary knowledge and the writer’s projections)

For the second mannequin, I appeared on the common variety of shops opened lately and noticed that it was 20.5. I additionally appeared on the comparable same-store gross sales progress charge, which was 8.14%. For a extra conservative mannequin, I used 18 shops opened and seven% comparable same-store gross sales progress. Consequently, I bought a lot increased numbers than in my first mannequin.

Costco’s Estimates Income (Authored utilizing Costco monetary knowledge and the writer’s projections)

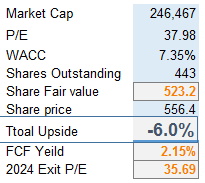

I additionally used a reduced money circulate (DCF) methodology to evaluate Costco’s truthful worth. For this mannequin, I assumed that the corporate’s income would develop at a compound annual progress charge (CAGR) of 9.1% between 2023 and 2030, based mostly on its robust warehouse enlargement and membership progress. That is a lot increased than the consensus forecast.

The valuation displays a 2024 P/E of 35.5x, based mostly on my EPS projection for 2024. That is according to the consensus.

Creator’s assumption (Created and calculated by the writer)

Primarily based on this mannequin, I estimate the corporate’s truthful worth to be $523.2 per share.

Dangers & challenges

Reliance on membership charges: Costco generates a good portion of its income from membership charges. If members resolve to cancel their memberships, it might harm the corporate’s backside line. Nonetheless, Costco reduces this danger by providing a high-value membership program with unique reductions, free transport, and different advantages. The corporate additionally has a really excessive membership renewal charge, which means that members are glad with the worth they obtain. Competitors: Costco faces competitors from different warehouse golf equipment, conventional grocers, and on-line retailers. Nonetheless, the corporate has an a variety of benefits, together with its robust model repute, environment friendly enterprise mannequin, loyal buyer base, and deal with higher-quality merchandise and a extra curated buying expertise. Altering shopper preferences: Client preferences are continuously altering, and Costco should adapt to maintain up. For instance, the rise of on-line buying has posed a problem to brick-and-mortar retailers. Nonetheless, Costco is adaptable and has invested closely in its e-commerce enterprise. The corporate additionally gives a variety of merchandise on-line and is increasing its number of recent produce and different wholesome meals choices. Rising prices: Costco’s prices might rise because of inflation, labor prices, and provide chain disruptions. This might result in decrease revenue margins or increased costs for purchasers. Nonetheless, Costco negotiates favorable contracts with suppliers and operates effectively to mitigate rising prices. The corporate additionally has a powerful monitor file of passing alongside value financial savings to prospects. World enlargement dangers: Costco’s international enlargement exposes it to dangers reminiscent of foreign money fluctuations, political instability, and cultural variations. Nonetheless, Costco fastidiously selects new markets and companions with native firms to mitigate these dangers. The corporate additionally has a powerful monitor file of success in worldwide markets.

This fall-2023

Primarily based on Costco’s robust third-quarter outcomes and historic seasonality, I anticipate the corporate to generate income of $77,228 million in This fall-23. That is barely under the consensus forecast, however it’s nonetheless a powerful efficiency contemplating the present financial atmosphere. Costco is well-positioned for progress in This fall-23 due to its deliberate enlargement in warehouse and e-commerce companies. The corporate can be benefiting from its loyal buyer base and its deal with providing worth and comfort. I additionally anticipate Costco to realize an working revenue margin of three.3% in This fall-23. That is barely decrease than the corporate’s historic margin, however it’s nonetheless a decent efficiency given the rising prices of labor and supplies.

After adjusting my mannequin to mirror COST’s Q3-23 outcomes, I now venture that the corporate will generate full-year income of $240,579 million in 2023. This represents a progress of 6% from the corporate’s income in 2022.

When the This fall-23 report comes out, I’ll publish a follow-up article with an up to date mannequin, so keep tuned!

Conclusion

Costco is a well-managed firm with a powerful monitor file of progress. The corporate has a novel enterprise mannequin that’s based mostly on membership charges and low costs. Costco’s membership renewal charge is extraordinarily excessive, which is a testomony to the worth that the corporate gives to its members.

Costco is going through some challenges, reminiscent of rising prices and competitors from on-line retailers. Nonetheless, the corporate is well-positioned to beat these challenges and proceed to develop sooner or later. Costco has a loyal buyer base, a powerful model, and a administration workforce that’s targeted on long-term progress.

I consider that Costco is an effective funding for buyers who’re searching for an organization with a powerful monitor file of progress and a shiny future. However, for now, I like to recommend a maintain ranking. I’m assured that Costco will proceed to be a pacesetter within the warehouse membership business for a few years to come back.

[ad_2]

Source link

{kind=link}