[ad_1]

Greenback cruises increased, nonfarm payrolls on Friday shall be essential for this rallyEarly indicators level to a different strong month for the US labor marketCentral financial institution choices in Australia and New Zealand will even be in focusDollar goes on a rampage

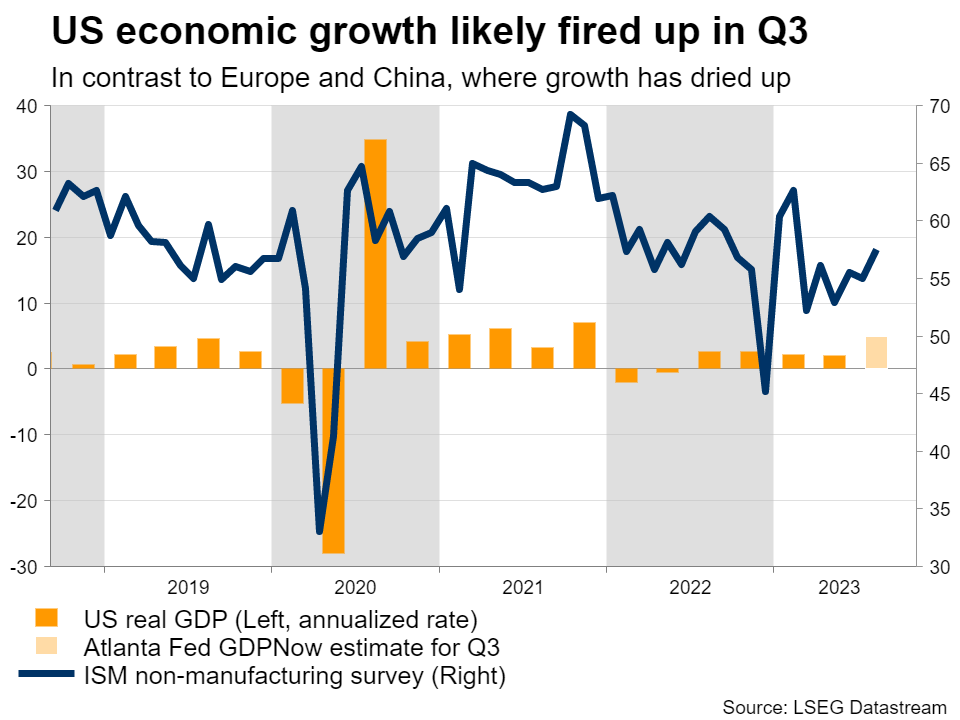

The US greenback rally has gone into overdrive recently. Empowered by a surprising rise in US yields, strong financial fundamentals, and protected haven flows, the greenback has charged increased to file 11 consecutive weeks of positive factors towards the euro.

In a nutshell, america seems far more resilient than every other area. Incoming information releases proceed to reaffirm the power of the US financial system, whereas in distinction, Europe is struggling a pointy slowdown in financial progress and China remains to be coping with the implosion of its property sector.

This differential in financial progress is more and more pushing traders in the direction of america, and the spectacular rally in US yields recently has made the greenback much more enticing from an rate of interest perspective.

Therefore, the greenback presents the ‘full bundle’ in the mean time – the very best actual charges among the many main economies, the strongest financial progress, and protected haven qualities because of its reserve foreign money standing. In the meantime, there’s a scarcity of enticing options within the FX area, as each different main foreign money is coping with its personal issues.

Subsequent week’s information releases will both add extra gasoline to this rally or set off a correction, with the principle occasion being the US employment report on Friday. Forecasts counsel nonfarm payrolls rose by 150k in September, lower than the earlier month however nonetheless a good quantity general. In the meantime, the unemployment charge is projected to have ticked again down to three.7%, whereas wage progress is predicted to have picked up some steam in month-to-month phrases. If the forecasts are met, this could be one more dataset reinforcing the Fed’s message that rates of interest may stay increased for longer.

As for any surprises, most early indicators level to a different strong month for the US labor market. Purposes for unemployment advantages fell sharply in September, so there have been no indicators of any mass employee layoffs. Equally, enterprise surveys from S&P International signaled a reacceleration in employment progress.

Talking of enterprise surveys, the ISM manufacturing index is due on Monday, forward of the non-manufacturing PMI on Wednesday. Within the political scene, the federal government will shut down this weekend except a funding deal is reached in Congress. That stated, markets normally ignore these shutdowns, as traders view them as political theater. For markets to care, it will have to be a protracted shutdown that dampens financial progress.

RBA and RBNZ choices

Crossing into Australia, the Reserve Financial institution will conclude its assembly early on Tuesday, the primary one below the brand new Governor, Michelle Bullock. Although information releases have been quite robust recently, with the labor market having fun with a considerable restoration in August and inflation reaccelerating, markets assign lower than a ten% likelihood to a charge improve.

That’s principally as a result of the most recent alerts from the central financial institution itself present a desire for retaining charges unchanged. The newest RBA minutes preached endurance, as charges have already risen shortly and the total influence of all this tightening has not been felt but.

A choice to maintain charges unchanged would argue for a damaging response within the Australian greenback, however nothing dramatic, as that is the market’s baseline state of affairs already.

In neighboring New Zealand, the central financial institution will announce its personal resolution on Wednesday. The market-implied likelihood for a charge improve can be round 10%, but it surely would possibly nonetheless be an thrilling occasion because the financial system has outperformed expectations recently. Therefore, the query is whether or not the RBNZ will set the stage for one more charge hike in November.

Inflation appears to be gaining momentum once more. Although inflation cooled slightly within the second quarter, the roles market remained very tight, with file ranges of labor power participation and an explosion in inhabitants progress serving to to spice up demand. As well as, the depreciation of the New Zealand greenback in latest months coupled with the sharp rise in oil costs will even assist to refuel inflation.

Towards this backdrop, the RBNZ will possible maintain charges unchanged, however maybe sign {that a} charge improve in November is an actual risk. Markets assign a 60% likelihood to that state of affairs, and if this likelihood strikes any increased within the aftermath, it may elevate the foreign money considerably.

That stated, there’s an election in two weeks, so the danger is that the RBNZ doesn’t ship any clear alerts, to keep away from interfering. Both method, the final outlook for the greenback appears grim, even when the foreign money spikes increased after the RBNZ. The slowdown in international progress and the deterioration in threat sentiment will possible maintain a lid on any rallies.

Chinese language information releases shall be in focus too. China is the biggest buying and selling associate of each Australia and New Zealand, so these currencies are very delicate to developments in China, the place the most recent enterprise surveys shall be launched over the weekend.

Elsewhere, Japan’s Tankan enterprise survey for Q3 will hit the markets on Monday, whereas in Canada, the employment report for September will see the sunshine on Friday.

[ad_2]

Source link