[ad_1]

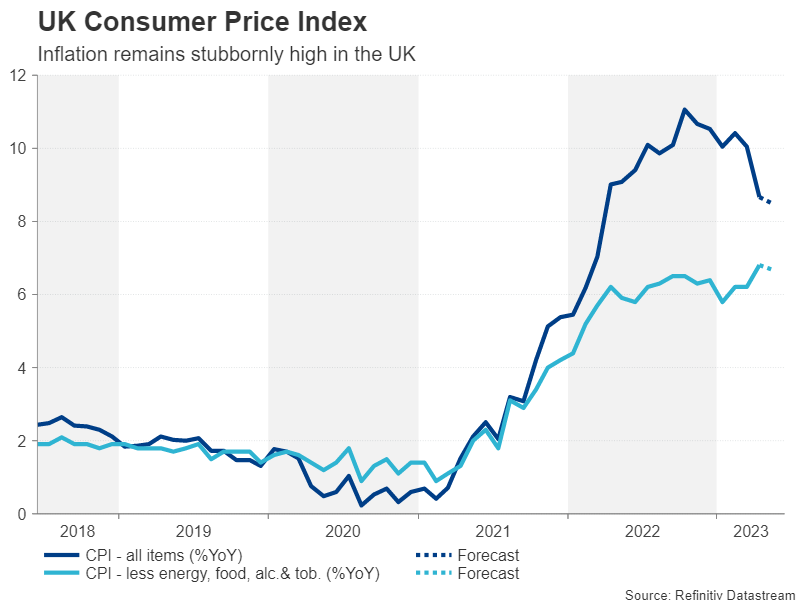

Stress is constructing on policymakers to get a grip on inflation quick after each wage development and underlying costs pressures began to warmth up once more lately, dashing hopes for a pause. Fortuitously for the Financial Coverage Committee (MPC), they are going to have some assistance on Tuesday after they get their palms on the newest CPI report earlier than voting the next day.

Headline inflation is anticipated to have moderated additional in Might, declining to eight.5% y/y. Nonetheless, even when there’s one other sizeable drop in headline CPI, policymakers will probably be extra involved in regards to the core measure. After capturing as much as 6.8% in April, core CPI is anticipated to have inched marginally decrease to six.7% in Might, suggesting there’s one other wave of second-round results underway.

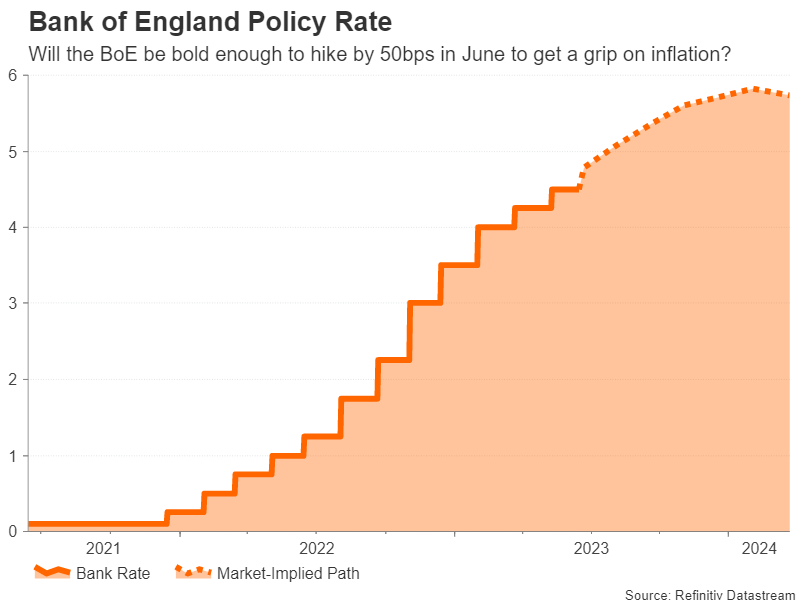

If the CPI figures are hotter-than-expected, which might come on the again of a robust employment report, the Financial institution of England would possibly properly resolve to lift rates of interest by a bigger 50-basis-point increment. Nonetheless, the probabilities of which might be fairly low. Traders have assigned only a 12% likelihood of a 50-bps hike and the BoE has not gone towards the markets through the course of this tightening cycle besides when it shocked at liftoff.

The MPC will most likely level to the lag impact of its current coverage tightening in addition to the dangers to the housing market if it raises the Financial institution fee by solely 25 bps as anticipated on Thursday. There is no such thing as a press convention or up to date forecasts on the June assembly however any adjustments to the language within the assertion that flags extra fee will increase can be constructive for the pound.

Even when the BoE offers little away about its intentions at future conferences, sterling may gain advantage from a broadly constructive set of information, as retail gross sales numbers for Might are additionally due on Friday, together with the flash PMIs for June.

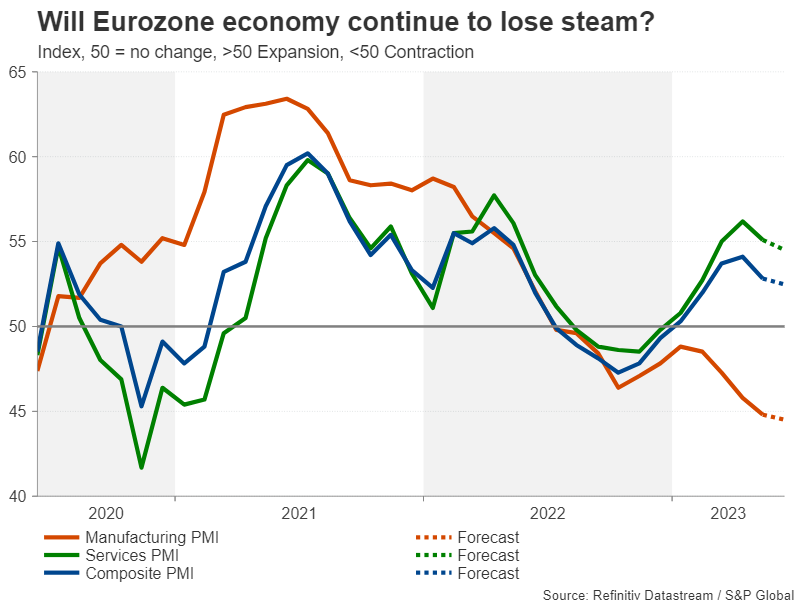

Will Eurozone PMIs soothe recession woes? Throughout the channel, the flash PMIs will take centre stage within the euro space as doubts develop in regards to the resilience of the bloc’s economic system after revised GDP estimates put the Eurozone in a technical recession. To date, the recession tag hasn’t led to a big shift in market expectations about additional tightening from the European Central Financial institution as development in Q1 was dragged decrease by poor efficiency in a small variety of nations, together with Germany, however different economies continued to develop.

The preliminary PMI readings for June ought to give some thought as as to whether this gentle downturn is popping into one thing deeper or if financial exercise in locations like Germany is beginning to rebound.

The euro might recognize towards the US greenback from any upside surprises within the manufacturing and companies PMIs, particularly after the ECB hiked charges this week and signalled they should go even greater, whereas the Fed saved its coverage settings unchanged.

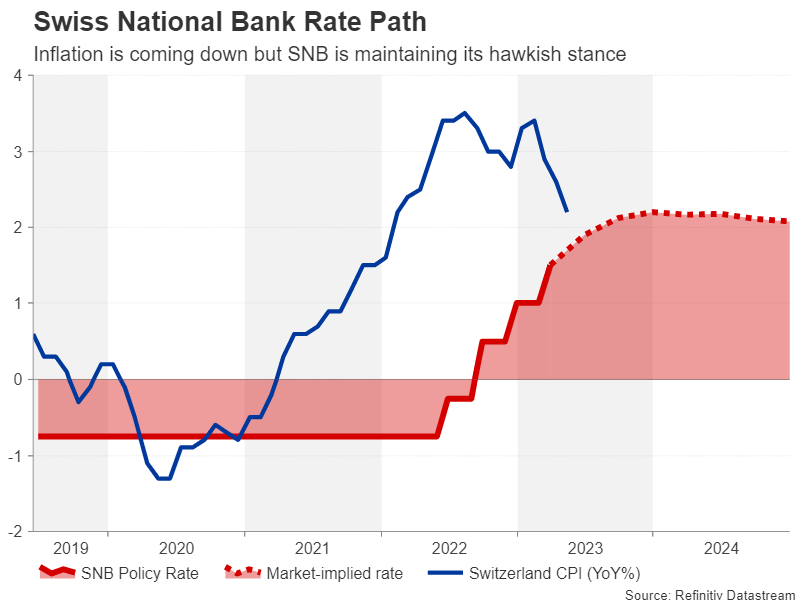

However towards the Swiss franc, the only foreign money would possibly wrestle ought to the Swiss Nationwide Financial institution observe go well with and elevate charges subsequent week.

SNB not finished elevating ratesThe odds of a 50-bps hike by the SNB on Thursday went up after unusually hawkish language from Chairman Thomas Jordan lately. The hawkish rhetoric comes even if inflation in Switzerland fell to 2.2% in Might, a lot to the envy of different nations.

Nonetheless, the SNB doesn’t appear to assume that coverage is restrictive sufficient because it desires to see inflation fall under 2%. Policymakers may additionally be fearful in regards to the fall in CPI being momentary and contemplating that the SNB meets solely 4 occasions a yr, a 50-bps hike appears extra probably.

If that seems to be the case, the franc might get pleasure from sturdy features as a 50-bps transfer is just about 60% priced in in the mean time. Although the dimensions of the increase would depend upon whether or not or not the SNB indicators additional tightening within the second half of the yr.

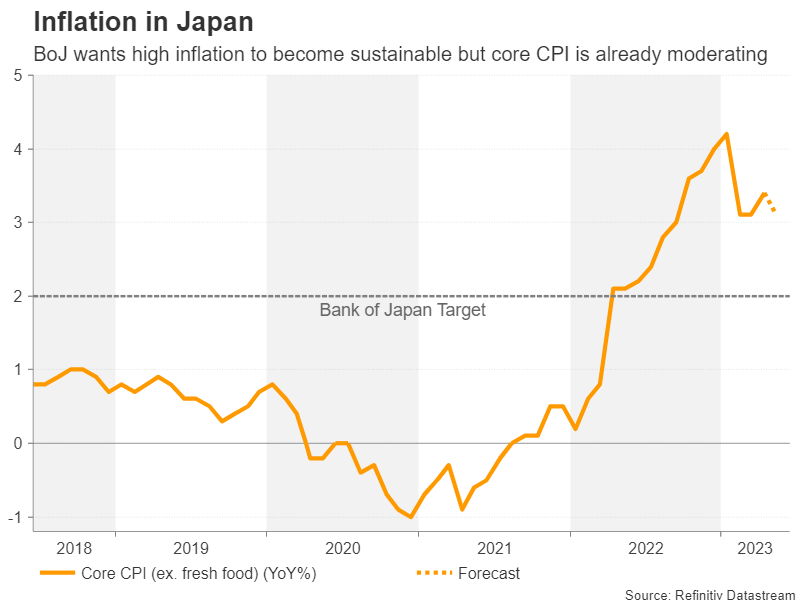

Japan’s reflation nonetheless has some option to goAnother nation the place the inflation downside has been extra manageable is Japan. After peaking at 4.2% in January, core CPI has eased considerably, though it did edge as much as 3.4% in April. It’s forecast to have eased to three.1% y/y in Might when the information is launched on Friday. From a coverage perspective, inflation doesn’t essentially need to climb to new peaks for the Financial institution of Japan to consider altering course and it solely wants to remain above 2% for an prolonged time period.

In the intervening time, nonetheless, the Financial institution of Japan is sustaining its easing stance because it desires to make sure that the pickup in costs and wages is sustainable. That is mirrored within the Japanese yen, which has tumbled sharply towards main currencies this month.

But, with many merchants pondering that it’s solely a matter of time earlier than the BoJ begins unwinding its large stimulus, the yen might start to indicate indicators of life ought to a clearer sample of persistent inflation start to type. Additionally to be careful of Japan subsequent week are Friday’s flash PMIs amid an upturn in financial development recently.

[ad_2]

Source link