[ad_1]

Delmaine Donson/E+ by way of Getty Pictures

Introduction

Intra-Mobile Therapies (NASDAQ:ITCI) develops novel therapies for neuropsychiatric and neurological circumstances by focusing on the central nervous system. Caplyta, their foremost drug, is FDA-approved for schizophrenia and bipolar despair in adults and is in section 3 trials for main depressive dysfunction.

In my current evaluation of Intra-Mobile Therapies, I highlighted the corporate’s promising potential because of the success of lumateperone, particularly in treating blended options in neuropsychiatric circumstances. The anticipated MDD approval and development of Caplyta indicated sturdy funding potential. Nevertheless, their reliance on Caplyta for income posed dangers, particularly with exclusivity expiration. Regardless of these challenges, the corporate’s numerous pipeline and sturdy money place, paired with optimistic future prospects, led me to improve their inventory from “Maintain” to “Purchase”.

The next article evaluations Intra-Mobile Therapies’ potential and challenges. Highlighting Caplyta’s success in treating neuropsychiatric circumstances, it discusses financials, development methods, dangers, and maintains a “Purchase” suggestion.

Q2 2023 Earnings

Taking a look at Intra-Mobile’s most up-to-date earnings report, complete revenues for Q2 2023 reached $110.8M, a considerable rise from $55.6M in Q2 2022. This development was primarily pushed by Caplyta’s web product gross sales, which doubled year-over-year to $110.1M. Regardless of the elevated income, the corporate recorded a web lack of $42.8M, an enchancment from the $86.6M loss in the identical quarter of the earlier yr. Value of product gross sales grew to $7.2M from $4.7M. SG&A bills remained comparatively steady at $101M, whereas R&D bills noticed a major uptick to $49.8M, primarily as a result of greater lumateperone venture prices. The corporate boasted a wholesome money place, with $514.6M available as of June 30, 2023. For the total yr, Caplyta gross sales steering was adjusted upwards to a spread of $445M to $465M.

Liquidity & Stability Sheet

Turning to Intra-Mobile Therapies’ stability sheet, the corporate’s present liquidity place consists of money and money equivalents of $142.25M and funding securities available-for-sale amounting to $370.60M, summing as much as a complete of $512.85M. From the Condensed Consolidated Statements of Operations, the corporate reported a loss from operations of $95.57M during the last six months. Extrapolating this to an annualized foundation, we anticipate an approximate working lack of $191.14M. Given the liquidity place, the money runway is about 2.68 years ($512.85M ÷ $191.14M). The corporate’s general liquidity appears passable, with its present belongings considerably exceeding its present liabilities ($698.07M vs. $92.08M). There is a restricted quantity of legal responsibility on the stability sheet ($106.51M in complete liabilities), indicating low leverage. Nevertheless, if the corporate continues its present pattern of operational losses, it could require extra financing sooner or later to help its operations and any unexpected investments.

Valuation, Development, & Momentum

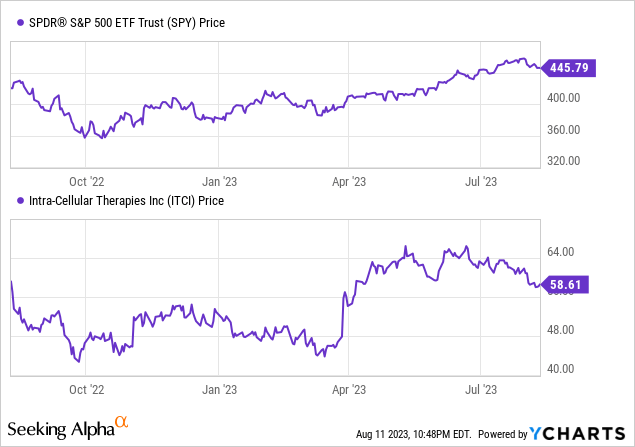

Based on In search of Alpha information: ITCI capital construction reveals a market cap of $5.59B with minimal debt and a wholesome money reserve, leading to an enterprise worth of $5.10B. Its valuation metrics are difficult to interpret given the non-meaningful P/E ratios, though it trades at a excessive Value/E book of 9.21 and has an elevated EV/Gross sales of 13.93. The corporate is experiencing sturdy development, with earnings estimates indicating a sturdy income enhance; the YoY gross sales development for 2023 is a formidable 84.06%, which is predicted to proceed rising over the subsequent few years. Regardless of the unfavorable momentum prior to now three months at -12.40%, the 6 and 9-month momentum are optimistic at +19.58% and +14.86% respectively, contrasting barely with the inventory’s minor decline over the yr.

Development Initiatives

Of their current earnings name, Intra-Mobile Therapies highlighted their development methods:

Lumateperone’s Broad Potential: The corporate emphasised the optimistic reception for Research 403 associated to lumateperone, which confirmed vital symptom discount for sufferers with blended options in temper issues. They plan to current these outcomes at upcoming psychiatric conferences and intention to interact the FDA for additional discussions.

Adjunctive MDD Program: Lumateperone is being evaluated as an adjunctive remedy for Main Depressive Dysfunction [MDD] in three ongoing Section 3 research. Outcomes for 2 of those trials are anticipated in 2024, with an anticipated submitting for supplemental new drug software [sNDA] later that yr.

Lumateperone Lengthy Appearing Injectable (LAI) Formulations: Plans are underway to start Section 1 research on a number of new LAI formulations, aiming for longer remedy durations.

Pipeline Growth:

ITI-1284: This yr, Section 2 applications will probably be initiated to judge ITI-1284 for generalized anxiousness dysfunction, psychosis in Alzheimer’s sufferers, and agitation in Alzheimer’s sufferers.

ITI-500 Sequence: Specializing in non-hallucinogenic psychedelics, the corporate developed novel compounds to harness therapeutic potentials with out the opposed results typical of identified psychedelics. Their lead compound, ITI-1549, will probably be evaluated in IND research, with human testing slated for late 2024 or early 2025.

PDE1 Inhibitors Platform: The continued Section 2 trial of Lenrispodun targets Parkinson’s illness signs, whereas ITI-1020, a most cancers immunotherapy candidate, is in a Section 1 examine.

ITI-333: Designed for opioid use dysfunction and ache remedy, ITI-333 has accomplished a single ascending dose examine, with outcomes from a number of ascending dose research anticipated in 2024.

My Evaluation & Advice

In analyzing the present standing and future trajectory of Intra-Mobile Therapies, a number of key observations emerge. The notable success of Caplyta, with its substantial development in web product gross sales, undoubtedly factors to a promising avenue for the corporate. The continued sturdy launch and reception of this drug, particularly its potential in addressing blended options in temper issues, are a testomony to the corporate’s dedication to innovation and affected person care.

From an investor’s standpoint, a number of components warrant shut statement within the coming weeks and months. The forthcoming outcomes from the Section 3 research on lumateperone’s adjunctive remedy for Main Depressive Dysfunction [MDD] could possibly be pivotal. Optimistic outcomes right here might additional solidify Caplyta’s place available in the market and doubtlessly pave the way in which for prolonged indications. Moreover, given the projected development charges, how shut Intra-Mobile is to turning a revenue will probably be a matter of intense scrutiny. If present tendencies maintain, the hole between operational bills and revenues might slim considerably, bringing the corporate nearer to profitability.

Nevertheless, considerations persist. The corporate’s vital reliance on Caplyta for its income stream is perhaps considered as a double-edged sword. Whereas the drug’s success is driving development, any setbacks, particularly within the face of patent exclusivity expiration, might have disproportionate impacts on the corporate’s monetary well being. Additional, whereas the money runway suggests a buffer for the subsequent few years, sustained operational losses might compel the corporate to hunt extra financing – a transfer that all the time comes with its share of complexities and potential dilutions for present shareholders.

In gentle of the above, and the corporate’s clear course in increasing its neuropsychiatry choices – from the exploration of non-hallucinogenic psychedelics to initiatives in Parkinson’s illness and opioid use dysfunction therapies – I stay optimistic. Thus, I preserve my “Purchase” suggestion for Intra-Mobile Therapies. The rationale hinges on Caplyta’s promising prospects, the corporate’s numerous and revolutionary pipeline, and its sturdy money place, which collectively place it nicely to navigate future challenges and capitalize on alternatives.

[ad_2]

Source link

{kind=link}